With interest rates near historic lows, investors have started to explore more exotic options to increase portfolio yield. One common area that has seen large amounts of interest over the past several years is emerging market debt, which refers to any debt securities issued in countries considered to be “emerging” such as China, South Korea, India, Brazil, and Mexico. Emerging market (EM) debt has some favorable characteristics as an asset class, as well as its own share of risks. The properties of this asset class and its role in a portfolio will be the subject of this Investment Product Review.

Emerging market debt most commonly comes in the form of bonds, issued by sovereign treasuries, quasi-sovereign entities (such as government agencies), and EM corporations. Until the early 1990s, it was nearly impossible for EM governments to issue debt in their own currency; they generally had to sell debt issued in “hard” currencies (typically the dollar or the euro). However, as many of these countries have become better established, and investors have grown comfortable with the idea of “developing” economies, EM countries have begun to issue an increasing portion of sovereign debt in their own currency, commonly referred to as local currency debt. At present, the majority of sovereign debt is denominated in local currency, though quasi-sovereign and corporate bonds are nearly always issued in US dollars.

As with EM equities, the characteristics of the debt issuers can vary greatly from country to country. For example, countries like China (AA- debt rating from Standard & Poor’s) and Korea (A+) are considered to be relatively safe issuers, while countries like Turkey (BB+) and Greece (B-) are considered more speculative. While the risk of default is nearly non-existent for sovereign bonds issued by countries like the US or Germany, defaults are not unheard of in emerging economies. Argentina (technically a “frontier” market rather than emerging) has defaulted on its debt 7 times in the last 200 years, including as recently as 2001, and is considered a serious threat to default again in the next year or two. Even stable corporations in emerging countries are subject to country-specific risks, such as political instability or even government confiscation of company assets.

Because there are a set of risks associated with emerging market bonds that are not generally present with the debt of developed countries, investors tend to command a higher premium to hold EM debt, which comes in the form of a higher yield to maturity. The spread between yields of EM bonds and US Treasury bonds of similar maturities tends to be around 4-6% annually. This spread is relatively similar for local currency and hard currency bonds, as relative currency movements are unpredictable and result in fairly symmetric payoffs (meaning that they can either hurt or help the investor, depending on which direction the exchange rate moves).

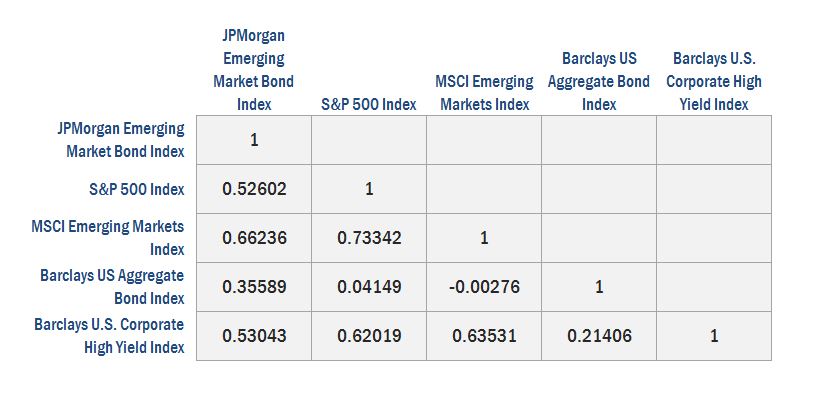

Aside from the higher yields (and thus higher expected returns), another attractive feature of EM debt is the diversification it has historically offered. The following table1 shows the correlations between emerging market bonds and other asset classes over the previous 20 years ending in 2013.

As can be seen in the above table, EM debt tends to move more closely with EM equities than with US bonds. This can be a mixed blessing, as bonds are primarily used in a portfolio to temper equity volatility. It can be beneficial to hold securities that stabilize a fixed income portfolio, but holding bonds that fall in value when equities are struggling can compound damage to a portfolio.

Emerging markets can often conjure visions of poor villagers living in primitive huts and scraping a living out of the land, but it should be noted that as of 2011 emerging and frontier countries accounted for 83% of the global population and 48% of world GDP. Despite this, EM securities make up less than 15% of global market capitalization. In addition, while some EM countries have well-documented fiscal instability, many others have much lower government debt burdens than developed countries like the United States. Taking these factors into consideration, emerging markets exhibit many characteristics that would imply that they have favorable prospects over the long term.

In summary, emerging market debt can provide higher yields in a fixed income portfolio, as well as diversification. However, it can be a risky asset class, and may add equity-like risk to bond holdings. An allocation to EM debt can be beneficial to an investor with a long time horizon who is willing to accept moderate amounts of risk, but should not be used simply for “chasing yield” in a portfolio. Investment risk is generally better rewarded in equity than in fixed income, and high dividend/coupon income is rarely the most efficient way to maximize portfolio returns. For an investor who has the capacity and tolerance for short-term volatility, EM debt can enhance portfolio returns and may in fact reduce portfolio drawdown through diversification. Once the decision is made to invest in EM debt, the investor must consider the preferred method (i.e. sovereign versus corporate) and whether or not to take currency risk. As with all risky securities, investors will likely be rewarded over long periods of time for EM debt exposure, as long as it makes sense in the context of their portfolio and they are able to create and commit to a long-term investment strategy.