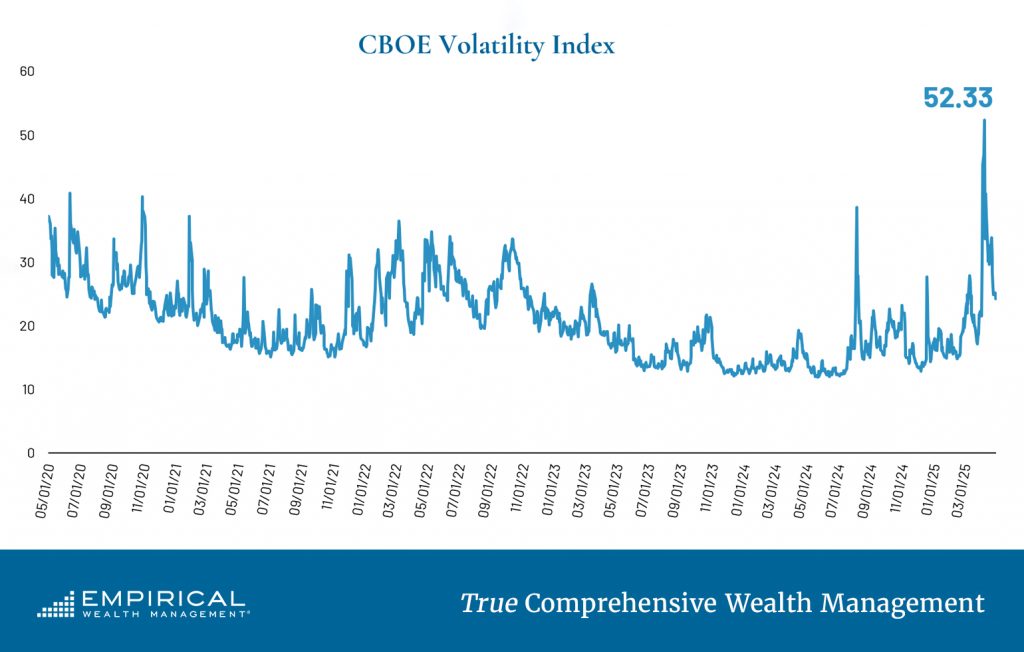

After a long stretch of calm, volatility has returned to financial markets. Recent tariff announcements have triggered sharp fluctuations in asset prices. The Volatility Index (VIX), a measure of market-wide price changes, spiked as stocks sold off, briefly crossing 50 in early April. That level has not been reached since the early days of the COVID crisis. For much of the past few years, markets remained steady, with the exception of a sharp disruption in August 2024.

Market downturns often prompt a familiar question: is this a buying opportunity or the beginning of a more serious correction? At Empirical Wealth Management, we view these periods through the lens of historical market data.

As of late April, the MSCI All Country World Index (ACWI) is 6% below its February high. The S&P 500 has declined 10% from its peak. While declines like these may seem unsettling, they are typical. Since 1950, the S&P 500 has closed at an all-time high on only 8% of trading days. The index has spent 52% of the time at least 5% below its high, 36% of the time 10% below, and 16% of the time 20% or more below its peak.

In short, the current environment is not unusual. This may be surprising, but it is important context for long-term investors. Our research also shows that the average intra-year decline since 1950 has been 13.6%. By comparison, the recent 19% sell-off in the S&P 500, while sharp, is within the bounds of past experience. Negative headlines may have amplified the emotional toll, but not the historical significance.

Investor behavior often reflects emotion rather than discipline, especially during periods of volatility. Selling during sharp declines may offer short-term relief but can be costly over time. Market volatility is a normal part of investing and should be expected. It does not mean a strategy has failed. For long-term investors, it may represent a chance to reinforce their plans, not abandon them.

Looking back at the S&P 500’s historical performance, the market has produced positive returns 74% of the time over any one-year period and 84% of the time over any three-year period. Notably, the odds of future gains increase after periods of steep declines. One- and three-year forward returns have historically improved with deeper drawdowns.

At Empirical, we believe that perspective matters. Our investment approach is guided by historical evidence and informed by rigorous analysis. Remaining disciplined, diversified, and invested has rewarded investors over time. Volatility, while uncomfortable, has consistently served as the engine for long-term returns. Those who stay invested through turbulent periods are more likely to benefit when markets recover.