The low-interest-rate environment following the Global Financial Crisis led many investors to seek alternative sources of bond yields. Debt securities issued in emerging markets (EM), such as China, India, Brazil, and Mexico, saw a rapid increase in investor interest. These large economies are well-integrated into the global economy and benefit from fast-growing production levels and industrialization. Debt issued by emerging markets has favorable characteristics as an asset class, along with its own risks. This Investment Product Review will examine the properties of emerging market debt and its role in a diversified portfolio.

What is Emerging Market Debt?

Emerging market debt primarily consists of bonds issued by sovereign treasuries, quasi-sovereign entities (such as government agencies), and EM corporations. Until the early 1990s, EM governments rarely issued debt in their own currency, typically opting for “hard” currencies like the US dollar. However, as these countries’ capital markets matured and investors grew more comfortable with “developing” economies, EM countries began issuing more sovereign debt in local currencies. Today, the majority of sovereign debt is denominated in local currency, while quasi-sovereign and corporate bonds are nearly always issued in US dollars.

Characteristics and Risks of Emerging Market Debt

Similar to EM equities, the characteristics of debt issuers vary greatly from country to country. For example, countries like China and South Korea, both rated A+ by Standard & Poor’s, are considered relatively safe issuers. In contrast, countries like Turkey (BB+) and Greece (B-) are deemed more speculative. While the risk of default is nearly non-existent for sovereign bonds issued by stable countries like the US or Germany, defaults are not unheard of in emerging economies. Argentina, for example, has defaulted on its debt nine times in the last 200 years, including as recently as 2020, and narrowly avoided another default in 2023. Even stable corporations in emerging markets are subject to country-specific risks, such as political instability or weak property rights.

Higher Yields and Risk Premiums

Because of the unique risks associated with emerging market bonds, investors typically demand a higher premium to hold EM debt, resulting in a higher yield to maturity. The spread between yields of EM bonds and US Treasury bonds of similar maturities is generally around 4-6% annually. This spread is similar for both local currency and hard currency bonds, as relative currency movements are unpredictable and can either benefit or hurt the investor, depending on exchange rate fluctuations.

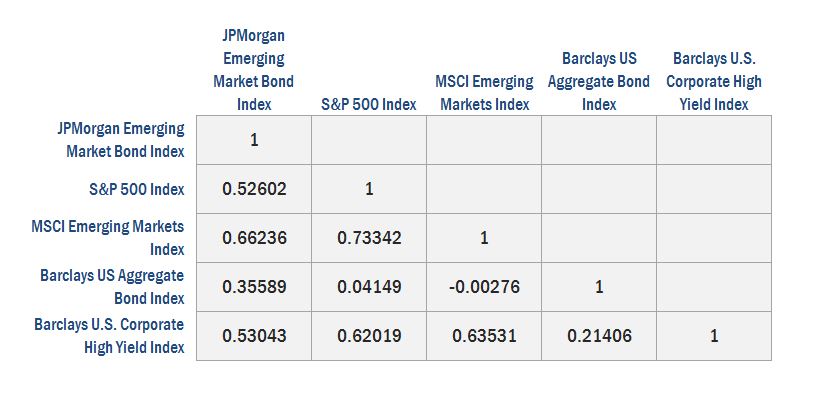

Diversification Benefits of EM Debt

Aside from higher yields and expected returns, another attractive feature of EM debt is the diversification it offers. The following table shows the correlations between emerging market bonds and other asset classes over the past 20 years, ending in 2023.

Source: FactSet as of 6/18/2024. All indices measured in USD total returns.

As the table indicates, EM debt tends to move more closely with EM equities and US high yield bonds than with US stocks. This correlation can be a mixed blessing, as bonds are generally used in a portfolio to temper equity volatility. While it can be beneficial to hold securities that stabilize a fixed income portfolio, holding bonds that fall in value when equities are struggling can compound portfolio losses.

Key Takeaways

In summary, emerging market debt can provide higher yields in a fixed income portfolio and offer diversification benefits. However, it can also add equity-like risk to bond holdings. An allocation to EM debt can be beneficial for investors with a longer time horizon and a willingness to accept moderate amounts of risk but should not be used solely for “chasing yield.” Investment risk is typically better rewarded in equity than in fixed income, and high dividend/coupon income is rarely the most efficient way to maximize portfolio returns.

For investors with the capacity and tolerance for short-term volatility, EM debt can enhance portfolio returns and may reduce drawdown through diversification. Once the decision is made to invest in EM debt, investors must consider the preferred method (i.e., sovereign versus corporate) and whether to take on currency risk. As with all risky securities, long-term exposure to EM debt can be rewarding if it fits within the context of the investor’s portfolio and aligns with a long-term investment strategy.

For investors looking to enhance their portfolios with emerging market bonds, contact Empirical Wealth Management. We can help you navigate your investment choices and make informed decisions for a secure financial future.